{kind=link}

Venture capital funding represents the fuel that powers the world’s most ambitious ideas, turning sketches on napkins into global empires that redefine how we live and work. I remember sitting in a dimly lit coffee shop in Palo Alto a few years ago, listening to a founder explain her vision for a decentralized energy grid. She had the brilliance and the data, but her bank account was nearly empty. That is the paradox of innovation; the most revolutionary ideas often require the most capital before they can even prove they work. For her, and for thousands like her, the path to success isn’t just about hard work but about navigating the complex, often opaque world of institutional investment.

Securing this type of investment is rarely a straightforward transaction of money for equity. It is more akin to a high-stakes marriage that lasts for a decade or more. When a founder accepts venture capital funding, they are bringing on a partner who will sit in their boardroom, influence their hiring decisions, and push for aggressive growth at all costs. This relationship can be the catalyst for legendary success, but it also introduces a level of pressure that many first-time entrepreneurs are unprepared for. It requires a fundamental shift in mindset from owning a small business to steering a rocket ship that is expected to reach the moon or crash in the attempt.

The history of this industry is rooted in a specific brand of courage—the willingness to lose everything for a chance at a “ten-bagger” return. In the mid-20th century, the first pioneers of the venture world began funding companies that traditional banks wouldn’t touch. These banks wanted collateral like buildings or machinery, but the new wave of tech founders only had intellectual property and ambition. Venture capitalists filled this gap, creating a model where they expected ninety percent of their bets to fail as long as one or two became the next Intel or Apple. This appetite for extreme risk is what differentiates this asset class from almost any other financial vehicle in existence.

Experience in this field teaches you that the “pitch” is only about twenty percent of the battle. The rest is about relationship building, timing, and an almost obsessive attention to market dynamics. I’ve seen founders with mediocre products raise millions because they understood the psychology of the investor, and I’ve seen geniuses fail because they couldn’t articulate their “moat” or their go-to-market strategy. It is a world of signals, where who you know and who introduces you can be just as important as the lines of code in your software.

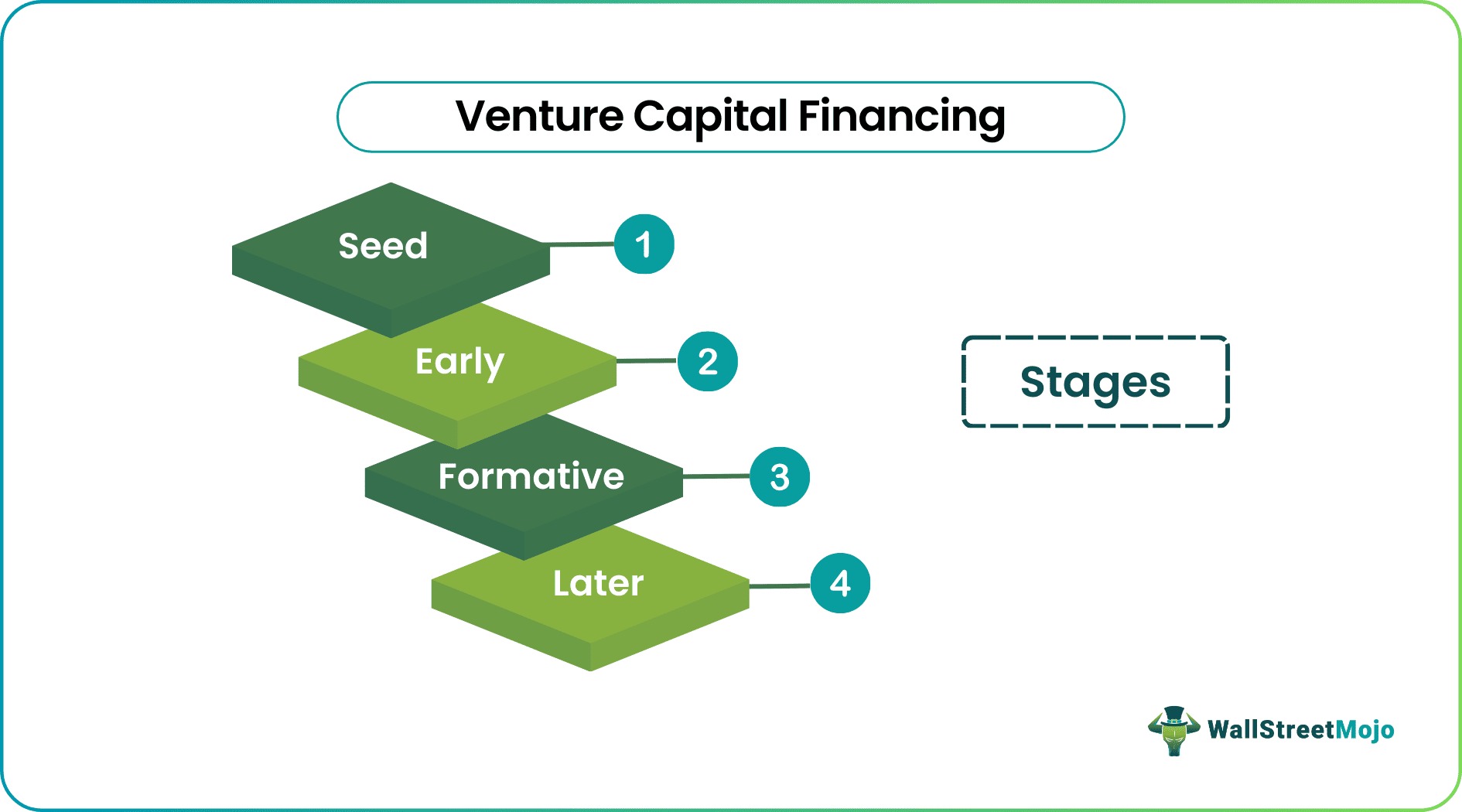

Navigating the phases of venture capital funding

Understanding the lifecycle of a startup is essential for any founder looking to attract professional investors. It usually begins at the “Seed” stage, where the focus is on proving that a problem exists and that your solution is viable. At this point, investors are betting more on the founder’s character and the size of the market than on actual revenue numbers. They want to see “founder-market fit,” which is the belief that this specific person is the only one in the world capable of winning this specific race. It is a period of intense experimentation, where the goal is simply to find “product-market fit” before the cash runs out.

As the company finds its footing, it moves into Series A, B, and C rounds. This is where the narrative shifts from “could this work?” to “how big can this get?” Series A is notoriously the most difficult hurdle to clear, as it requires the transition from a scrappy team to a functioning organization with predictable metrics. Investors at this stage are looking for “unit economics”—proof that for every dollar you spend on customer acquisition, you are getting three or more dollars back in lifetime value. If you can prove that the machine works, the venture world will provide the capital to turn the crank faster and faster.

Later stages, like Series C and beyond, are often about international expansion, acquisitions, and preparing for a potential exit through an IPO or a major sale. By this time, the original founders often find themselves with a much smaller percentage of the company than they started with, a process known as dilution. However, the hope is that a small piece of a multi-billion dollar pie is worth infinitely more than a large piece of a failing dream. This trade-off is the core agreement of the venture world, and navigating it requires a deep understanding of capitalization tables and long-term financial planning.

The recent shifts in the global economy have changed the rules of the game significantly. For a few years, we saw an era of “growth at all costs,” where companies were rewarded for burning massive amounts of cash to gain market share. However, the current trend has shifted back toward “path to profitability.” Investors are no longer impressed by raw user numbers if there isn’t a clear and sustainable way to make money. This return to fundamentals has been painful for many startups that were built on the old model, but it is creating a healthier ecosystem where only the most resilient and efficient companies survive.

The hidden risks of venture capital funding

While the headlines usually celebrate massive funding rounds, the reality under the surface is often much more complicated. One of the primary risks that founders overlook is the “liquidation preference.” This is a clause in the term sheet that dictates who gets paid first when the company is sold. In many cases, the venture capitalists get their money back before the founders or employees see a single cent. If a company raises too much money at too high a valuation and then sells for a lower price, the founders can walk away with nothing despite having built a successful business. This is the “downside protection” that investors use to mitigate their risk.

Another hidden danger is the loss of control. Most venture capital funding comes with board seats and “protective provisions” that give investors the power to veto certain decisions. This might include blocking a sale, preventing a new round of funding, or even firing the CEO. I have seen many founders who were “voted out” of their own companies because their vision no longer aligned with the investors’ desire for a quick exit. This tension is inherent in the model; the founder is building a legacy, but the investor is managing a fund with a ten-year expiration date.

The pressure to “scale” can also be a double-edged sword. When you have tens of millions of dollars in the bank, the temptation is to hire hundreds of people and spend heavily on marketing. But if you haven’t truly figured out your product yet, this “premature scaling” is the number one cause of startup failure. It is like putting a massive engine on a car that doesn’t have a steering wheel. You will go very fast, but you will almost certainly hit a wall. Founders must have the discipline to say “no” to spending, even when their investors are pushing them to grow faster.

There is also a psychological toll that comes with managing other people’s money. When it is your own savings, you can pivot or slow down whenever you want. When it is the pension funds of teachers or the endowments of universities—which is where most VC money actually comes from—the weight of responsibility can be crushing. Every decision is scrutinized, and every quarterly report is a trial. This environment requires a level of emotional resilience that isn’t often discussed in the glossy tech magazines, but it is the reality for every successful founder I know.

To build a trustworthy and authoritative presence in this space, one must also look at the “due diligence” process from both sides. Investors will spend weeks or months digging into your code, talking to your customers, and background-checking your team. They are looking for “red flags” that might suggest the business is built on a shaky foundation. As a founder, you should be doing the same. You need to talk to other founders in that VC’s portfolio, especially those whose companies failed. How did the investor act when things went wrong? Were they supportive, or did they immediately look for someone to blame?

Expertise in fundraising also means knowing when to walk away from a deal. Not all money is created equal. “Smart money” comes from investors who have deep connections in your industry, who can help you recruit top talent, and who can open doors to massive customers. “Dumb money” is just a wire transfer without any added value. In many cases, it is better to take a slightly lower valuation from a world-class partner than a higher valuation from someone who doesn’t understand your business and will only cause headaches in the boardroom.

The term sheet itself is a masterclass in legal and financial complexity. Beyond just the valuation, there are terms like “anti-dilution,” “participation rights,” and “drag-along rights.” Each of these can have a massive impact on your future. For instance, a “full ratchet” anti-dilution clause can essentially wipe out a founder’s equity if the company has to raise a “down round” at a lower valuation. Founders who don’t hire an experienced startup lawyer to navigate these waters are setting themselves up for disaster. You are not just signing for a check; you are signing the constitution of your company.

The relationship between the venture world and the broader economy is also a fascinating study in cycles. When interest rates are low, investors flock to venture capital in search of high returns, leading to an explosion of funding and high valuations. When interest rates rise, capital becomes “expensive,” and the flow of money into startups slows to a trickle. We are currently in a period of recalibration, where the “froth” is being washed out of the market. This is actually a great time to start a company, as there is less competition for talent and the founders who do manage to raise money are held to a much higher standard of excellence.

Diligence is not just about the numbers; it is about the “intangibles.” I’ve sat in rooms where a deal fell through because the investor didn’t like how the CEO treated the waiter at lunch. They are looking for “high integrity” because they know they are going to be in the trenches with you for a long time. They want to know that when the inevitable crisis hits, you won’t cut corners or lie to the board. Trust is the currency of the venture world, and once it is lost, it is almost impossible to regain.

The role of the “Lead Investor” is another critical concept to master. This is the firm that sets the terms, does the bulk of the due diligence, and usually takes a board seat. Once you have a lead, the rest of the round often fills up quickly as “follow-on” investors jump in, a phenomenon often called “FOMO” or fear of missing out. The challenge is getting that first “yes.” It requires a combination of a compelling vision, undeniable data, and a bit of theater. You have to convince the investor that the train is leaving the station and they are lucky to have a ticket.

As the ecosystem matures, we are seeing more diverse sources of capital, including corporate venture capital, where large companies like Google or Intel invest in startups that are strategic to their business. This can be a huge win for a startup, as it provides an immediate “vouch” from an industry giant. However, it can also complicate your future if you want to sell to one of their competitors. Every choice in the funding world comes with a set of trade-offs that must be carefully weighed against your long-term goals.

The “exit” is the ultimate goal of the venture model. Whether it is an acquisition by a larger company or an initial public offering on the stock market, the goal is to provide a “liquidity event” for the investors and the founders. This is the moment when the paper wealth becomes real money. But reaching this stage is statistically rare; less than one percent of startups ever achieve a “unicorn” valuation of over a billion dollars. This reality check is important because it highlights that venture capital funding is not a badge of honor or a guarantee of success. It is simply a tool—a very powerful and dangerous tool that must be handled with extreme care.

Experience shows that the founders who stay grounded are the ones who succeed in the long run. They treat the funding as a responsibility rather than a windfall. They continue to focus on solving their customers’ problems rather than obsessing over their next valuation. They understand that while the money is important, the team, the culture, and the product are what actually build value. The venture world loves a visionary, but they respect a “grinder” who can execute on that vision day in and day out, regardless of the market conditions.

The future of this industry is likely to be shaped by “democratization.” New regulations and platforms are making it easier for smaller “angel” investors to participate in rounds that were previously reserved for the elite firms on Sand Hill Road. This could lead to a more diverse range of founders getting funded, particularly those from underrepresented backgrounds or geographic regions outside of the traditional tech hubs. This is a positive development for innovation, as great ideas can come from anywhere, not just from those who attended a handful of prestigious universities.

Ultimately, the journey of raising capital is a test of your conviction. If you don’t believe in your company enough to survive a hundred “no”s, then you probably aren’t ready for the “yes.” It is an exhausting, emotional, and often humbling process that will reveal your strengths and weaknesses in equal measure. But for those who have a vision that can change the world and the grit to see it through, the venture capital world offers a path to greatness that is unlike any other. It is the engine of the modern economy, and for the right founder, it is the opportunity of a lifetime.

The most successful entrepreneurs I’ve met are those who view their investors as mentors and advisors, not just sources of cash. They are transparent about their failures and proactive about asking for help. This level of communication builds the “trustworthiness” that is essential for a long-term partnership. When the investor feels like they are part of the team, they are much more likely to pull out their rolodex and go to bat for you when things get tough. It turns a financial arrangement into a shared mission.

Every round of funding is a milestone, but it is not the destination. The real work begins the day the money hits the bank. Now you have the resources to build what you promised, and the clock is officially ticking. The expectations have been set, the stakes have been raised, and the eyes of your investors are on you. It is time to stop pitching and start building. This transition is the true test of leadership, and it is where the real stories of innovation are written, one day at a time, in the quiet hours of hard work that follow the big announcement.

As the landscape continues to evolve, the fundamentals remain the same. Build something people want, surround yourself with a great team, and be honest about your progress. Whether you are seeking venture capital funding or bootstrapping your way to success, those principles will never go out of style. The venture world is just a high-octane version of the same game we’ve been playing since the first merchants traded goods across the ocean. It is about risk, reward, and the enduring power of a great idea to change the course of history.

Read also :-

| young18gye |

| miofragia |

| qapoxerfemoz |